Affordable housing is defined in the NPPF as follows:

The Government carried out a consultation in December 2015, proposing that the definition be expanded so as to include

– low cost ownership models, which “would include products that are analogous to low cost market housing or intermediate rent, such as discount market sales or innovative rent to buy housing”

– starter homes (of which more later).

Two further changes were proposed in the February 2017 response to consultation:

* introduction of a household income eligibility cap of £80,000 (£90,000 for London) on starter homes.

* introduction of affordable private rented housing

The Government is accordingly consulting until 2 May 2017 on the following replacement definition for the NPPF (long isn’t it?):

Starter homes

There were howls of anguish at the starter homes initiative as first unveiled by the Government, the key elements of which were (as set out in chapter 1 of the Housing and Planning Act 2016 and March 2016 technical consultation):

– a legal requirement that 20% of new homes in developments should be starter homes, ie

– to be sold at a discount of at least 20% to open market value to first time buyers aged under 40.

– Price cap of £250,000 (£450,000 in London)

– The restriction should last for a defined number of years, the first suggestion being five years, replaced with the concept of a tapered restriction to potentially eight years

– Commuted sums in lieu of on site provision for specified categories of development, eg build to rent

The obvious consequence would have been a significant reduction in the potential for schemes to include a meaningful proportion of traditional forms of affordable housing.

After all of last year’s battles over the Bill, it is now plain from the Government’s response to the technical consultation, that the starter home concept is now much watered down:

– There will be no statutory requirement on local planning authorities to secure starter homes, just a policy requirement in the NPPF, which is to be amended accordingly.

– Rather than requiring that 20% of new homes be starter homes, the requirement will be that 10% of new homes will be “affordable housing home ownership products” so could include shared equity or indeed low cost home ownership.

– maximum eligible household income of £80,000 a year or less (or £90,000 a year or less in Greater London

– 15 year restriction

– No cash buyers, evidence of mortgage of at least 25% loan to value

– It will only be applicable to schemes of ten units or more (or on sites of more than 0.5h).

There will be a transitional period of 18 months (to August 2018) rather than the initially intended 6 to 12 months.

Whilst we now have a more workable arrangement, plainly all that Parliamentary work was a complete waste of time. There was no need for chapter 1 of the 2016 Act – the current proposals can be delivered without any need for legislation.

We will need to see the degree to which LPAs embrace the starter homes concept in reviewing their local plans. We will also need to be wary that we may lose the only benefit of a national standardised approach, ie the hope that there might be a standard set of section 106 clauses defining the operation of the mechanism (which will not be straightforward – see my 21.6.16 blog post Valuing Starter Homes).

Affordable Private Rent

One of the documents accompanying the Housing White Paper was a consultation paper: Planning and affordable housing for build to rent.

The term Affordable Private Rent is now used for what we have all previously been calling Discounted Market Rent. Changes to the NPPF are proposed (subject to consultation) advising LPAs to consider asking for Affordable Private Rent in place of other forms of affordable housing in Build to Rent schemes, comprising a minimum of 20% of the homes in the development, at a minimum of 20% discount to local market rent (excluding use of comparables within the scheme itself), provided in perpetuity. The Affordable Private Rent housing would be tenure blind and representative of the development in terms of numbers of bedrooms. Eligible income bands are to be negotiated between developer and LPA. Developers will be able to offer alternative approaches where appropriate (eg greater discount, fewer discounted homes – or different tenures). “Build to Rent” will be defined and it is acknowledged that developers should be able to cease to operate the property as Build To Rent subject to payment of a commuted sum reflecting the affordable housing requirement that would otherwise have been applicable.

There is also recognition in the consultation paper that factors in London may be different, allowing for an amended response and recognition of Mayor of London’s November 2016 affordable housing and viability draft SPG.

There will be a transitional period of 6 months from the time that the NPPF changes are made. The possibility is held out of model section 106 clauses, which would help minimise unnecessary delays.

The recognition that Build to Rent is a model that doesn’t sit well with ‘ownership’ forms of affordable housing is what that industry (largely self-defining through scale of scheme and extent of professional management) has been lobbying for. Nor is there any more any reference to off-site starter home provision.

Wider implications

The extensions to the meaning of ‘affordable housing’ are all in the direction of private sector provision. The definition is now very wide indeed. Battles lie ahead once LPAs consider the implications of the changes for their local plan affordable housing requirements against a backdrop of, for example:

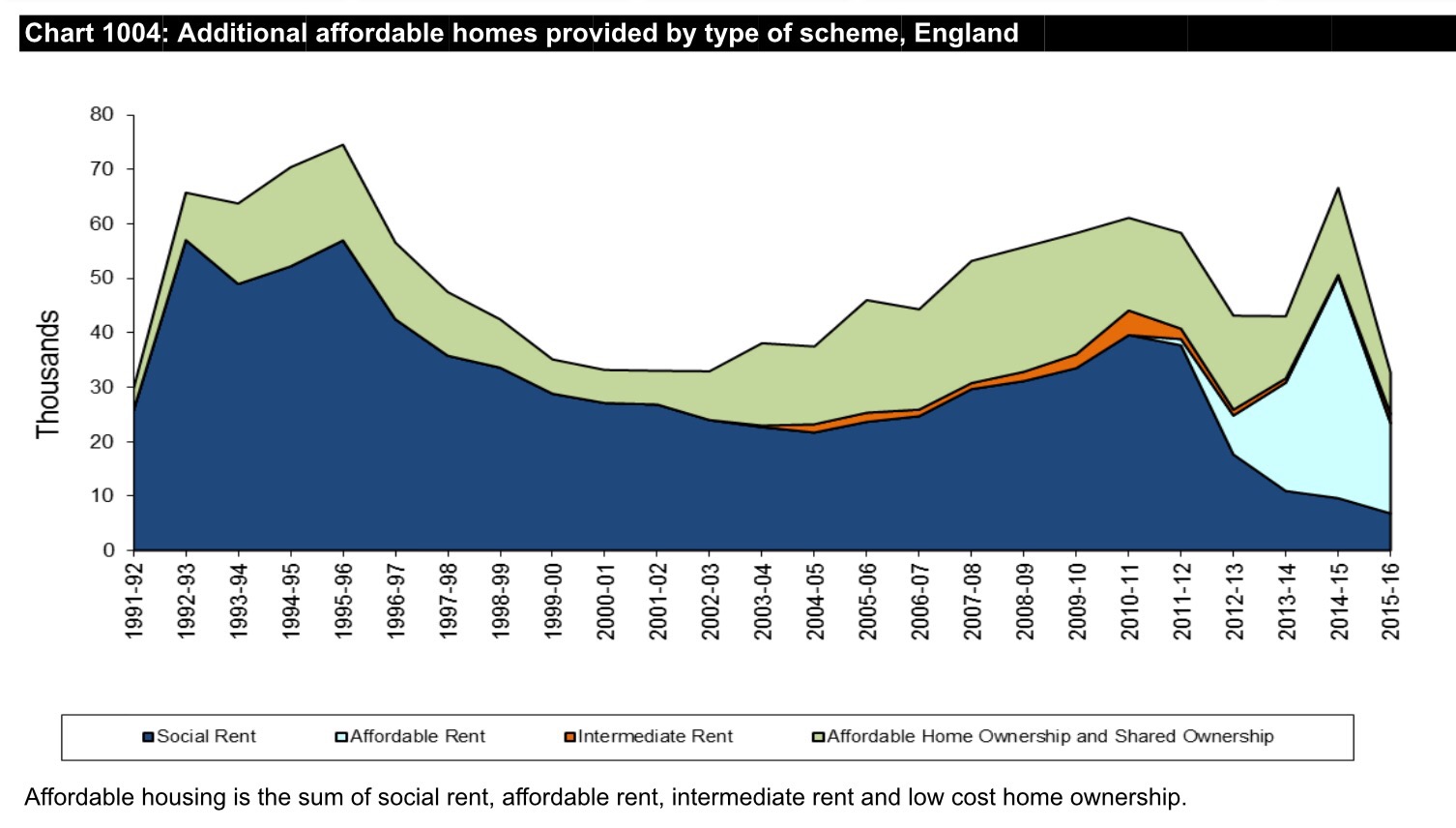

– reduced levels of socially rented housing over the last six years or so following the introduction of affordable rent (minimum discount of at least 20% to market rent), vividly demonstrated in the Government’s affordable housing statistics published on 2 March 2017:

– restrictions on housing benefit, for instance ineligibility of 18-21 year olds from 1 April 2017 under the Universal Credit (Housing Costs Element for claimants aged 18 to 21) (Amendment) Regulations 2017 made on 2 March 2017.

– the continuing, onerous, requirement on registered providers since 2015 to reduce rents by 1% a year for four years resulting in a 12% reduction in average rents by 2020-21.

– Loss of stock via the Housing and Planning Act 2016’s voluntary right to buy scheme in relation to registered providers and the Act’s provisions requiring local authorities to sell vacant higher value housing (the Government’s most recent statistics on sales date from October 2016 but already show significant numbers).

A debate took place in the House of Lords this week, on 2 March 2017, on the Economic Affairs Committee’s July 2016 report, Building More Homes in the context of the Housing White Paper. Lord Young closed for the Government saying many of the right things but, after such a background of continuing changes (I believe it was Adam Challis at JLL who recently counted 180 housing initiatives since 2010), with further uncertainty for at least 18 months, surely we now just need to get on with the matter in hand – ensuring that there are enough homes to meet all social needs, whilst not killing the golden goose without which this will simply not happen under any foreseeable system, ie profitable development by the private sector.

Simon Ricketts 4.3.17

Personal views, et cetera